QIMA 2023 Q1 Barometer

2022 in Review: No Slowing Down the Global Sourcing Rollercoaster

For the last three years, almost every new QIMA barometer would highlight a new wave of challenges facing global supply chains. 2022 was no exception, throwing the Russia-Ukraine geopolitical crisis with global repercussions into the sourcing landscape still struggling with logistics hurdles and reeling from the aftershocks of the COVID-19 pandemic. It is official: supply chain disruptions are here to stay for the foreseeable future, and QIMA 2022 data shows that during this seemingly never-ending storm, the fortunes of key buyer and supplier regions are ever-changing.

China’s Handling of COVID in 2022 Squanders Recovery Momentum and Damages Buyer Confidence

Throughout 2022, global supply chains with links to China were repeatedly rattled by the repercussions of the country’s “zero COVID” policy. After strict local lockdowns through most of the year, the lifting of restrictions in late 2022 raised initial hopes for normalized operations; instead, numerous virus outbreaks resulted in factory shutdowns, put further strain on the already struggling supply chains and created “eye-popping shortages” for major brands over the holiday season.

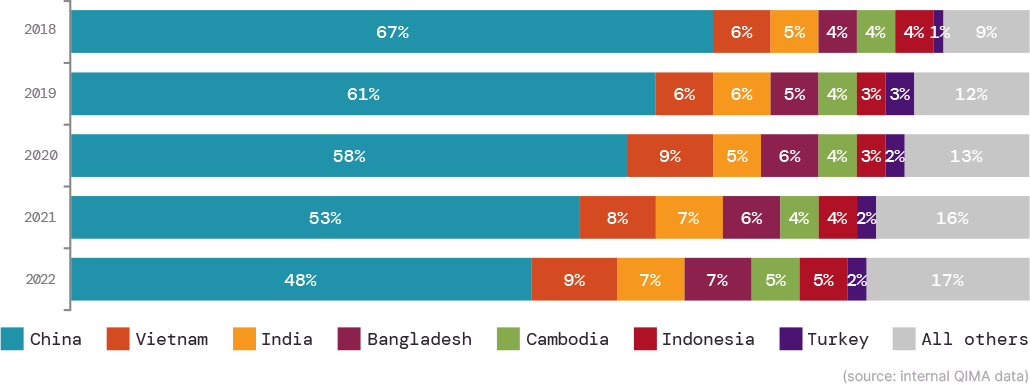

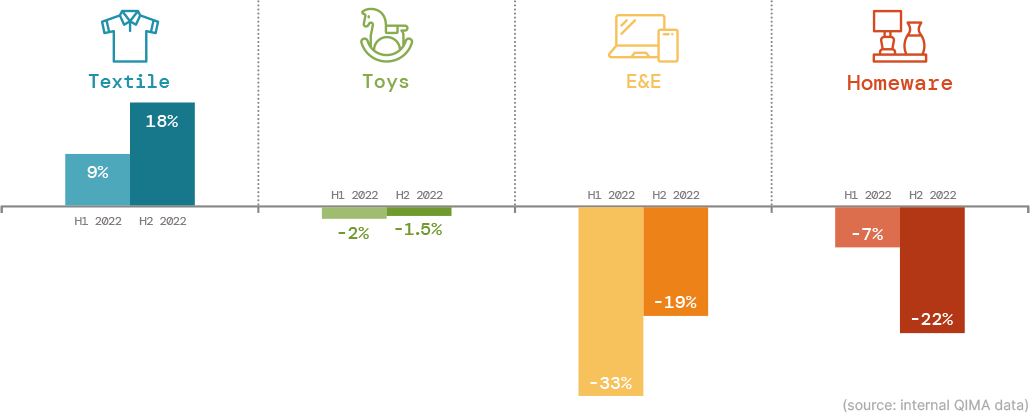

Analysts suggest that after 2022, business confidence in China has fallen to the lowest point in nearly a decade. QIMA data backs up this trend as far as the Western buyers are concerned: the relative share of China in the sourcing portfolios of Western companies is at a five-year low, based on aggregated QIMA data on inspection and audit demand; meanwhile, demand for inspections and audits from US and EU-based brands was down -10% YoY in 2022 (including a sharp -19% YoY slide in Q4). The decline in demand affects multiple product categories, including Homewares (-19% YoY from US and EU buyers) and the traditionally China-dominated Toys (-15% YoY).

Interestingly, buyers in other regions appear to be in less of a hurry to decouple from China, with inspection and audit demand from brands in Latin America and Asia in 2022 expanding +10% YoY and +23% YoY, respectively.

So where does this leave China in 2023? While US- and EU-based brands are likely to continue reducing their exposure to China sourcing by shifting volumes to its regional competitors and nearshoring alternatives, global supply chains remain tightly intertwined with the manufacturing giant, and China is likely to maintain its status as “the world’s factory” in the years to come.

Fig. C1. US and EU buyers’ top sourcing markets by share (source: internal QIMA data)

Fig. C2. 2021-2022 China inspection and audit YoY growth dynamic: selected industries, demand from buyers globally (source: internal QIMA data)

Southeast Asia Sees Strong Demand in 2022, with Vietnam in the Lead

Vietnam is possibly the best illustration of the exacerbated volatility in global supply chains these past couple of years: one year ago, the country was seeing its post-pandemic recovery hamstrung by staff shortages, and showing sluggish inspection and audit volumes, down -23% in Q4 ’21 compared to Q4 ’20. Fast forward a year later, Vietnam sourcing mounted a truly impressive comeback from Q3 2022 onward, finishing 2022 with +21.5% YoY growth in inspection and audit demand among global and Western buyers alike. The influx of new business into Vietnam was particularly pronounced in the third quarter, coinciding with one of the many waves of lockdowns in China. The ability to attract large swaths of orders from businesses wishing to reduce their reliance on China in 2022 played a big part in Vietnam concluding the year as the best-performing economy in Asia.

Among QIMA survey respondents, a third named Vietnam among their TOP3 sourcing partners in 2022; among those who diversified their supply chains in 2022, over a quarter chose to include more Vietnam sourcing in their buying geography.

Manufacturers elsewhere in Southeast Asia also remain eager to snap up opportunities from businesses shifting their buying out of China: QIMA data for 2022 shows double-digit expansion in demand for inspections and audits in Malaysia, Thailand, Cambodia, and the Philippines.

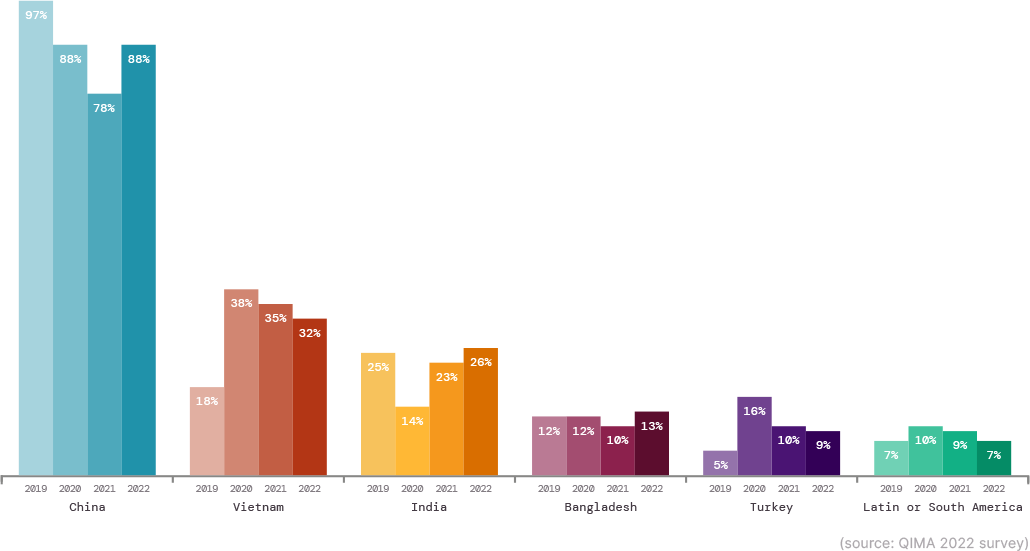

Fig. V1. Sourcing regions named among TOP3 by US+EU businesses (excluding home region) (source: QIMA 2022 survey)

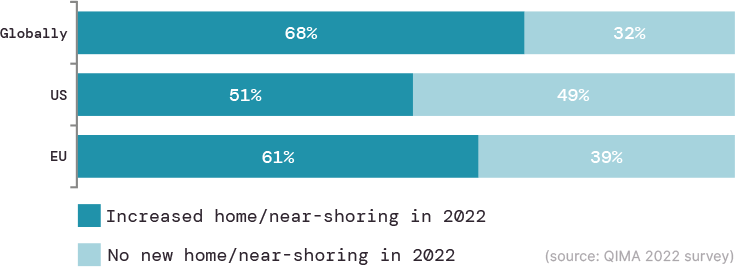

Appetite for Nearshoring Keeps Growing, with US Brands Now Picking Up the Pace

During 2022, brands and retailers with global supply chains have increasingly viewed nearshoring as an important component of supply chain diversification, even if volumes bought close to home are still firmly behind overseas procurement. Over half of US- and EU-based respondents of QIMA’s 2022 survey reported buying more from their home region in 2022, and 43% intend to keep nearshoring among their top sourcing strategies for 2023 and beyond.

While historically behind their EU counterparts on nearshoring, US brands have been increasingly casting their nets close to home in 2022, QIMA data shows. Mexico is a traditional go-to for US nearshoring, but other Latin American countries are not far behind: US buyers’ inspections and audits in Guatemala and Nicaragua shot up +23% YoY and 18% YoY respectively in 2022.

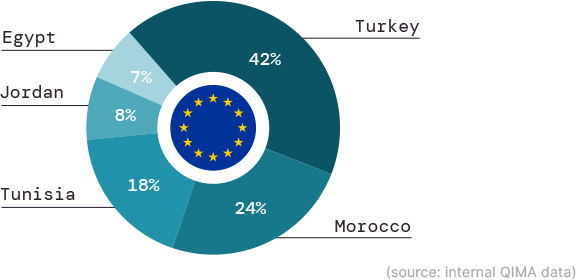

Meanwhile, among EU-based buyers, the appetite for nearshoring remains as high as ever, with double-digit growth for inspection and audit demand in multiple sourcing hubs around the Mediterranean, including Turkey (+36% YoY), Jordan (+28% YoY), Morocco (+19%), and Egypt (+12%). Combining the geographic proximity to Europe’s consumer markets with relatively low labor and energy costs, this region remains highly valuable for EU buyers, as shown by the fact that the combined share of the Mediterranean region in EU sourcing was higher than those of Bangladesh, India, or Vietnam.

Fig. N1. Nearshoring trends as reported by brands and retailers in 2022 (source: QIMA 2022 survey)

Fig. N2. Top EU sourcing markets in the Mediterranean, 2022 (source: internal QIMA data)

India Maintains Appeal as a Valued Partner for the West’s Diversification Efforts

Having been one of the biggest beneficiaries of the global drive to diversify supply chains in 2021, India stayed on a winning streak halfway into the year, before slowing down in H2 2022. Following several consecutive quarters of explosive growth, QIMA data shows demand for India inspections and audits settling at +8.5% YoY as of the end of 2022 (+5% YoY for US- and EU-based brands). While still a healthy growth rate (in line with South Asia as a whole at +8% YoY and slightly behind Bangladesh at +12% YoY), this slower expansion pace is a far cry from the double-digit year-on-year growth seen in late 2022-early 2021, being another example of the high volatility of today’s sourcing.

That said, India’s importance in the Western brands’ quest to diversify supply chains is likely to keep growing, owing to the country’s ongoing effort to broaden its horizons beyond the region’s traditional focus on textiles. Indeed, electronics giants including Apple and Google, are exploring sourcing opportunities in India: by some estimates, 5% of iPhone 14 production is expected to be moved to the country by early 2023, and the latest government policies aim to incentivize Apple to include India in its iPhone and MacBook value chains as well.

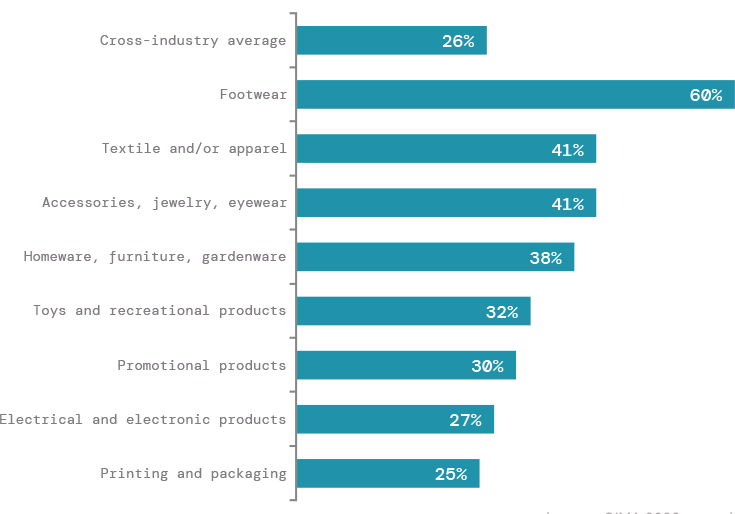

Fig. I1. US and EU businesses naming India as their TOP3 sourcing partner in 2022 – by industry (source: QIMA 2022 survey)

Despite Ongoing Disruptions, Businesses Cannot Afford to Drag Heels on Human Rights Due Diligence

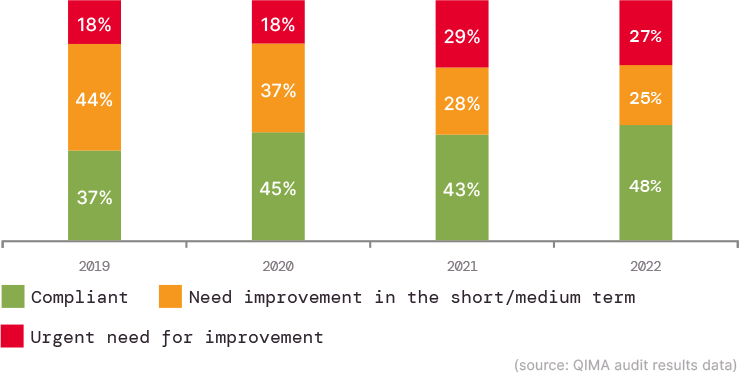

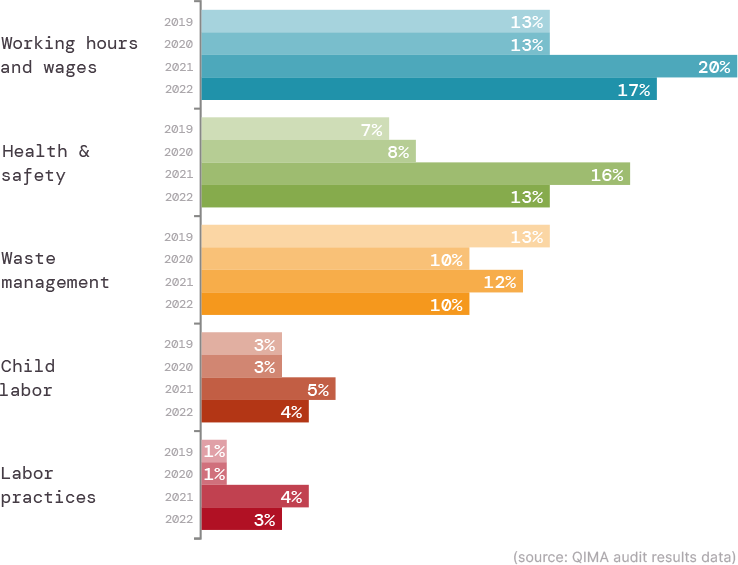

Data on ethical compliance of factories gathered by QIMA auditors during 2022 shows a mild uptick in factory ethical scores compared to 2021 averages, but it is too soon to tell whether this change represents sustained improvement. Overall, the frequency of critical violations across four out of the five key aspects assessed by QIMA auditors, including Health and Safety and Working Hours and Wages, remains above pre-pandemic levels, and more than half of all factories audited need improvement in the medium (25%) and immediate (27%) term.

Historically, ethical compliance tends to drop to the bottom of companies’ priority list during times of crisis, as buyers and suppliers alike are forced to prioritize cost concerns and operate in survival mode. However, as the current era of supply chain disruption is shaping up to be a new normal rather than a passing storm, businesses will have to find a way to move human rights and environmental compliance higher up on their agenda. Companies serving the EU market in particular cannot afford delays on this, with the EU Corporate Sustainability Due Diligence Directive adopted in late 2022 and the German Supply Chain Due Diligence Act coming into force this January.

Fig. E1. Evolution of factory rankings assigned by QIMA ethical auditors, 2019-2022 (source: QIMA audit results data)

Fig. E2. Percentage of factories with critical non-compliances by category, 2019-2022 (source: QIMA audit results data)

2023 Outlook: Supply Chains Must Balance Diversification with Strategic Sourcing Partnerships

As much, or even more than the preceding years, 2022 has highlighted the volatility of the global sourcing landscape, showing that even the strongest players are not immune from the rollercoaster driven by mounting disruptions of the pandemic, geopolitics, legislation, and climate change. China will be under particular scrutiny as the impact of the sudden lifting of COVID-19 restriction is hard to anticipate. To succeed in this new normal, businesses must focus on supply chain resilience, achieved by striking the right balance between the flexibility of diversification and the reliability of strategic supplier partnerships.

Press Contact

Email: press@qima.com